The Three Shifts That Changed the Math

If your factory is in Maharashtra, Karnataka, Gujarat, Tamil Nadu, or any of the 23 states where Time-of-Day tariffs are now mandatory for commercial and industrial consumers, the cost you pay for electricity between 6 PM and 10 PM has become one of the most volatile lines on your P&L. Not because of inflation. Because of regulation.

Three things changed in the last twelve months that should have your finance team’s attention.

The Maharashtra Electricity Regulatory Commission (MERC) issued its Modified Multi-Year Tariff Order in March 2025 (Case No. 217 of 2024), and after a Bombay High Court review and a follow-on order in June 2025 (Case No. 75 of 2025), the framework for High Tension Industrial consumers is now settled. Peak-hour consumption between 17:00 and 24:00 attracts a 20% surcharge on the energy charge. Solar-hour energy banked between 09:00 and 17:00 can only be drawn within the same time slot. And because the state’s rooftop solar capacity has crossed the 5,178 MW threshold, the Grid Support Charge has now been triggered.

The Government of Maharashtra notified the Renewable Energy and Energy Storage Policy 2025-26 to 2035-36 on 18 March 2026. From 1 April 2026, every new rooftop or grid-interactive solar project above 100 kW must integrate storage equal to at least 50% of the renewable capacity, with a minimum two-hour duration. The policy also exempts stored energy from cross-subsidy surcharge, wheeling charges, transmission charges, and electricity duty when consumed within the state. For projects with a four-hour BESS configuration, there is a 10-year electricity duty holiday on captive consumption.

The Central Electricity Regulatory Commission notified its Terms and Conditions of Tariff (Second Amendment) Regulations on 20 March 2026. The framework recognises Battery Energy Storage Systems as a regulated asset class with a 15-year useful life for lithium-ion systems, an 85% minimum round-trip efficiency requirement, and a 14% base Return on Equity for storage co-located with thermal generators or interstate transmission systems. While these specific provisions apply to utility-scale and ISTS-linked storage, the financial signaling effect for behind-the-meter Commercial and Industrial projects is significant. Banks now have a regulated tariff template to underwrite against.

What these three shifts have done, taken together, is convert the question of behind-the-meter battery storage from a sustainability decision into a finance decision. This blog is for the CFO, finance director, or plant head who has to make that decision in the next twelve months.

The Accounting Problem You Are Probably Not Solving For

Most industrial finance teams still treat the monthly electricity bill as a single line on the P&L. Under a flat-rate tariff regime, that was reasonable. Under Time-of-Day pricing, it is not.

A typical High Tension Industrial bill in Maharashtra has six distinct charge components. The base energy charge is the predictable one. The Time-of-Day surcharge of plus 20% during peak hours is a structural premium that re-prices every fiscal year through the MYT process. Wheeling charges, the cross-subsidy surcharge, electricity duty at 9.3% on the energy component, and the newly-triggered Grid Support Charge are administered levies, each set independently by the regulator and the state government.

Five of those six components behave less like fixed costs and more like floating-rate liabilities. They re-price annually. They trend upward. You have no negotiating leverage over them.

For a 2 MW HT Industrial plant in Maharashtra operating an evening shift, the annual peak-hour exposure works out to approximately ₹1.40 crore. That is cash leaving your business every year, with no underlying asset to show for it.

A CFO’s job is to convert volatile liabilities into fixed, depreciable obligations. That is the entire logic of the Avoided Cost Model.

What “Avoided Cost” Actually Means

Avoided cost, in finance-textbook terms, is the cost you no longer incur because you have deployed an alternative. In the Solar + BESS context, it has a precise definition: you do not buy peak-hour grid power at the regulated all-in rate. Instead, you discharge a battery that was charged from captive solar generation during the solar window, or from cheaper grid power during off-peak hours.

The delta between what you would have paid and what you now pay is not a saving in the colloquial sense. It is an avoided procurement cost that accrues every operating day for the 15-year life of the storage asset, and it qualifies as a depreciable capital expenditure on your balance sheet rather than a recurring expense on your P&L.

When the Avoided Cost Model is applied correctly, three things happen at once.

Electricity OpEx becomes partially fixed. The portion that used to float with ToD escalation, FPPA pass-throughs, and grid charges is now locked to the amortised cost of your storage asset, a number your team can pin down to two decimal places.

A capital asset appears on the balance sheet. Solar generation systems including integrated storage qualify as tangible fixed assets under Ind AS 16 and depreciate at 40% on Written Down Value in Year One under Section 32 of the Income Tax Act, with an additional 20% available in Year Two for assets put to use in manufacturing or power generation. (If commissioned after 3 October of a financial year, the Year One rate halves to 20%, so timing of commissioning matters.)

Forward EBITDA becomes more defensible. Lenders and analysts apply discount factors to volatile input costs. Removing that volatility from your cost base improves earnings quality even before you account for the absolute savings.

You are not “saving on the electricity bill.” You are reclassifying a volatile OpEx liability into a depreciating CapEx asset that pays its own coupon every operating day.

The Per-kWh Math, Honestly

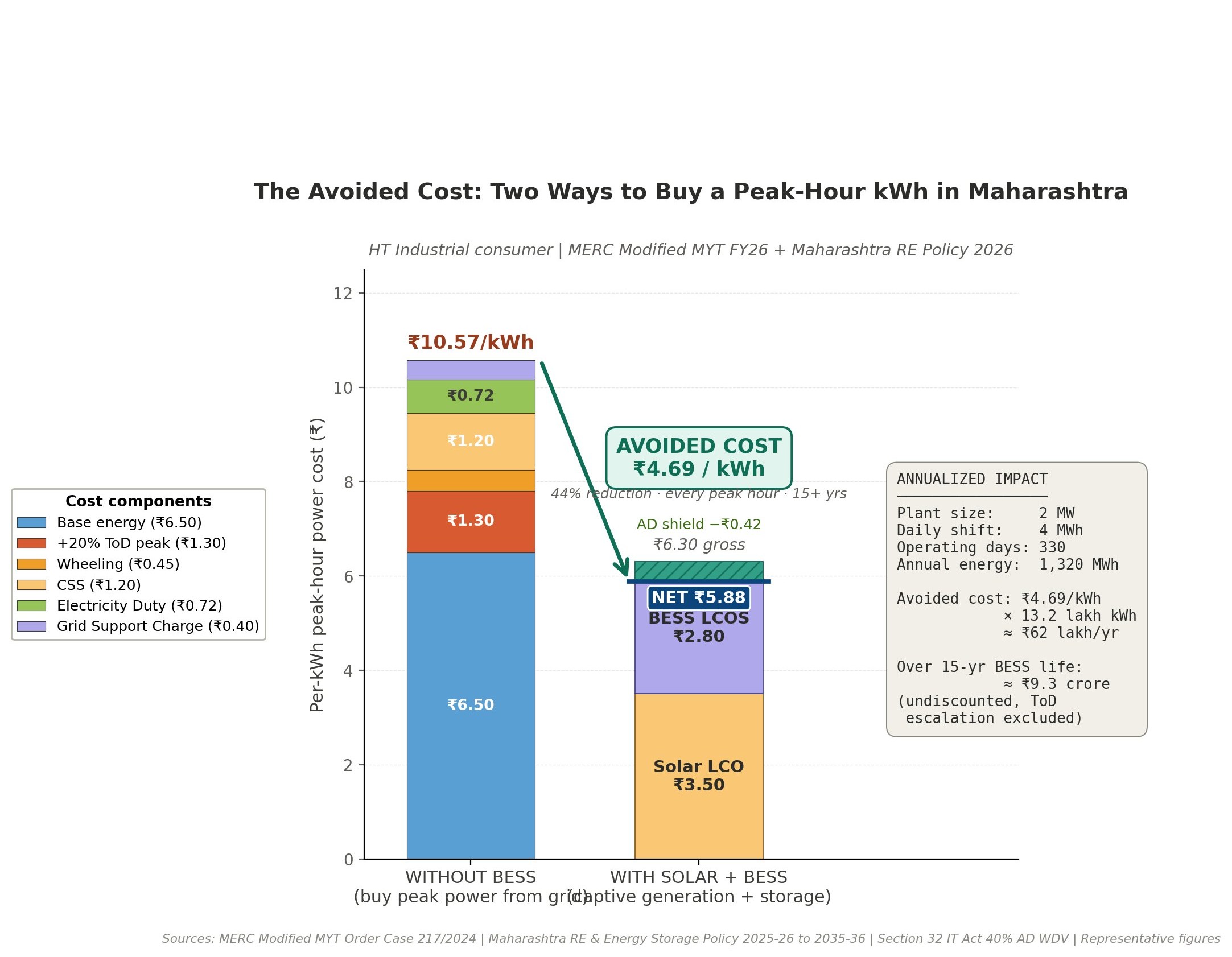

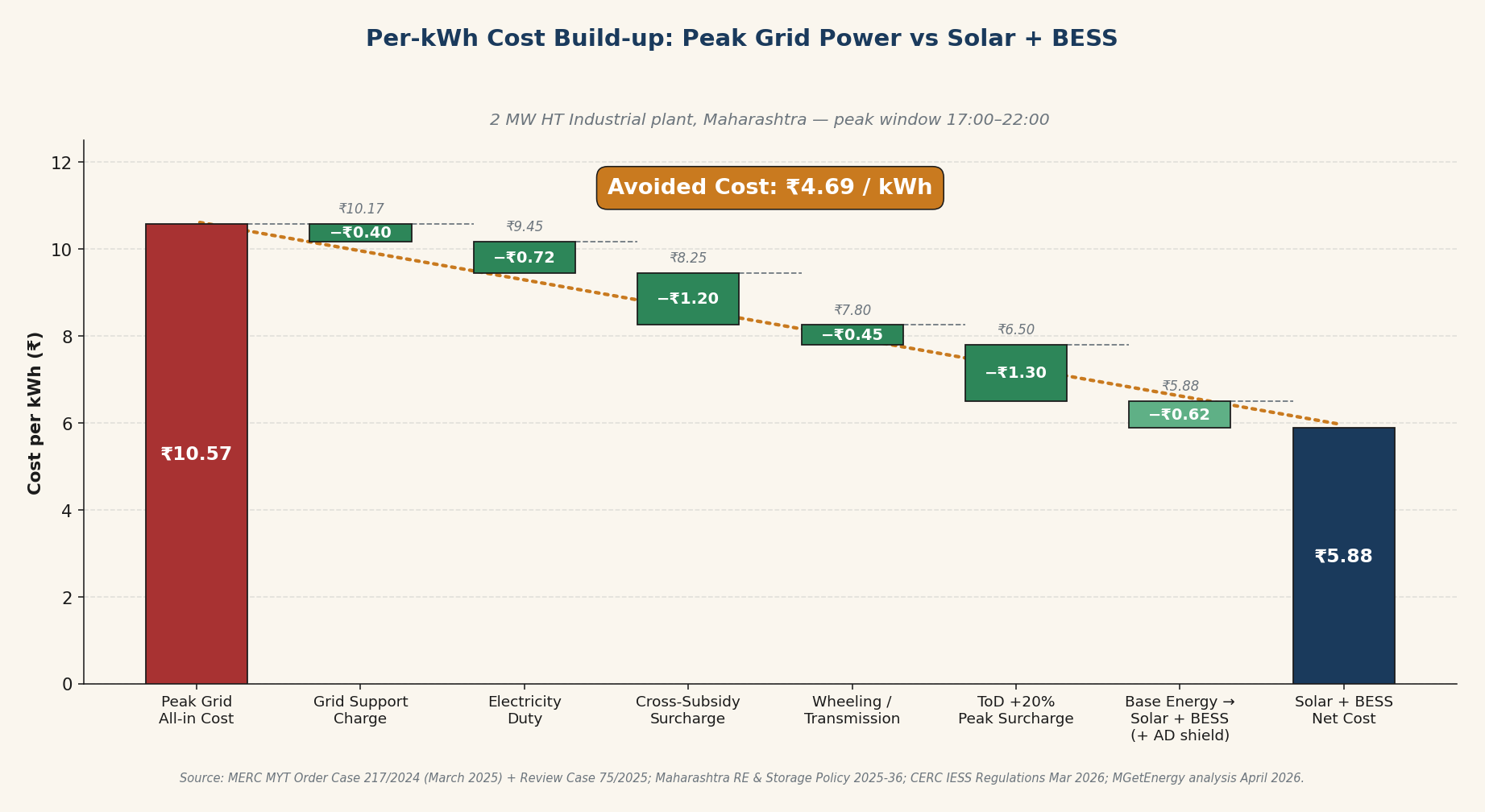

A peak-hour kWh of grid power for a Maharashtra HT Industrial consumer is built up from six layers, each set by a different regulatory mechanism. Five of those six are partially or fully avoidable through Solar + BESS. Here is what one peak-hour kWh actually costs in two scenarios for a representative 2 MW HT Industrial plant in Maharashtra (the per-kWh comparison is illustrated in the chart at the top of this article).

Without BESS, the all-in peak-hour cost is approximately ₹10.57 per kWh. The base energy charge of around ₹6.50 per kWh is the underlying cost of generation. The +20% ToD peak surcharge adds ₹1.30 per kWh. Wheeling and transmission charges add another ₹0.45 per kWh. The cross-subsidy surcharge adds ₹1.20, electricity duty adds ₹0.72, and the newly-triggered Grid Support Charge adds approximately ₹0.40 per kWh. The last four of these are now exempt for stored energy under the Maharashtra Renewable Energy and Energy Storage Policy 2025-36 when consumed within the state, and the +20% ToD surcharge is what you escape simply by shifting load from grid to battery during the peak window.

With Solar + BESS, the delivered cost of one kWh is the levelised cost of captive solar generation (around ₹3.50 per kWh, which is now stable across most C&I rooftop projects in 2026) plus the levelised cost of storage (around ₹2.80 per kWh, benchmarked against recent Indian utility-scale tenders that have cleared between ₹1.65 and ₹2.21 lakh per MW per month for two-hour stand-alone BESS). That delivers a gross stacked cost of ₹6.30 per kWh, against which the Year One accelerated depreciation tax shield contributes approximately ₹0.42 per kWh in tax-equivalent value, bringing the net effective cost to ₹5.88 per kWh.

Avoided cost: ₹4.69 per kWh, every peak hour, every operating day.

For a 2 MW plant shifting 4 MWh of load per day from peak to BESS-stored energy across 330 operating days, that translates to approximately ₹62 lakh of annual P&L impact from the peak-shift lever alone. Stack on demand charge reduction (around ₹15 lakh through kVA peak shaving), kVAh billing optimisation through power factor improvement (around ₹5 lakh on MSEDCL HT bills), and diesel generator displacement during outages (around ₹8 lakh), and the realistic annual benefit reaches ₹85-90 lakh.

Over the CERC-recognised 15-year useful life of the BESS, that compounds to roughly ₹15-17 crore of undiscounted cash flow, before any escalation adjustments for ToD surcharge growth.

The CFO’s Three Options Over Fifteen Years

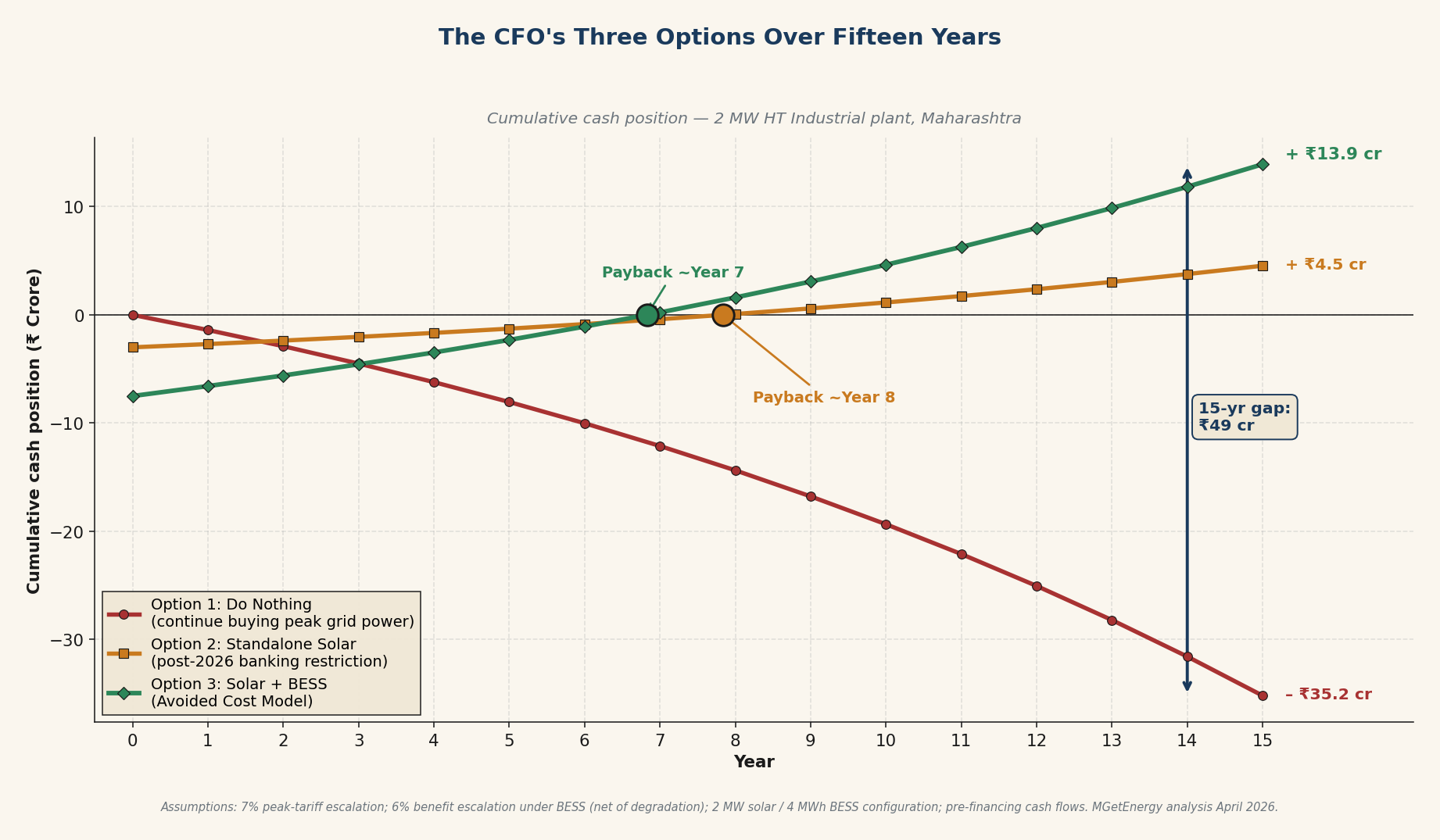

The real CFO question is not whether to do something. It is what each option does to your 15-year cash position. Run the numbers across three trajectories for a 2 MW HT Industrial plant in Maharashtra, and the gap between them is stark.

Option 1: Do nothing. Continue buying peak-hour power from the grid. At a conservative 7% CAGR on peak-tariff escalation, a 2 MW plant absorbs roughly ₹35 crore of cumulative peak-hour power cost over 15 years. That is ₹35 crore of cash written to the DISCOM, non-refundable, non-hedgeable, with no asset on your balance sheet to show for it. The cumulative cash outflow line trends steeply downward year after year, with no turning point.

Option 2: Standalone solar. Under the same-slot banking restriction now applicable in Maharashtra (and effectively similar provisions in Karnataka, Gujarat, and Rajasthan), solar banked during the 09:00 to 17:00 window can only be consumed within that same window. The peak-hour offset that drove the original Solar ROI math no longer works for new installations. Payback slips to Year 8, the 15-year cumulative gain is approximately ₹4.4 crore, and the plant continues carrying full peak-hour grid exposure through evening shifts. You stop the bleeding partially, but the peak-hour wound is still open.

Option 3: Solar + BESS under the Avoided Cost Model. Payback in Year 7. 15-year cumulative gain of approximately ₹13.75 crore. The difference between Option 3 and Option 2, roughly ₹9.35 crore over 15 years, is the specific value created by adding battery storage on top of solar in the post-2026 regulatory regime. The cumulative cash position curve crosses zero in Year 7 and trends sharply upward thereafter, while the Do Nothing curve continues its steep downward slide.

Plotted on a single chart, the three trajectories diverge so dramatically that the choice becomes self-evident. The cumulative gap between Option 1 and Option 3 over 15 years is approximately ₹48 crore — which is the answer to the question “what is the cost of doing nothing?”

A note of honesty: vendor proposals quoting 4-year paybacks for Solar + BESS projects usually omit financing costs, battery degradation (typically 2-3% annual capacity loss), commissioning delays, and realistic O&M over the asset life. Plan for 6-8 years on a properly modelled basis. The economics are still strong, but the framing matters when you present this to the board.

The Mandatory-or-Optional Question

For new Solar projects above 100 kW commissioned in Maharashtra from 1 April 2026, BESS is no longer optional. The Renewable Energy and Energy Storage Policy 2025-36 mandates storage of at least 50% of the renewable capacity with a two-hour minimum duration. A new 1 MW rooftop solar installation must now include at least 500 kW / 1,000 kWh of battery storage.

This mandate effectively converts the Avoided Cost Model from “should we?” to “since we have to anyway, how do we maximise the financial upside?”

For existing solar installations, the mandate does not retroactively apply. But the underlying economics, particularly the same-slot banking restriction and the ₹1.30 to ₹1.70 per kWh of grid charges that BESS-stored energy now escapes, mean that retrofitting BESS to an existing solar asset is increasingly the highest-IRR move available to a finance team that already has a solar plant on its books.

Three Other Levers Worth Naming

The Avoided Cost Model is the headline. Three secondary levers also deserve mention because they materially change the IRR calculation.

Demand charge reduction. MSEDCL bills HT consumers on Maximum Demand at ₹400 per kVA per month. A well-designed BESS can shave 0.5 to 1.0 MW off your monthly peak demand by discharging during high-load events. For a 2 MW plant, that translates to roughly ₹10-15 lakh per year in saved demand charges, independent of the peak-hour ToD arbitrage.

Power factor and kVAh billing. Maharashtra HT consumers are billed on kVAh consumption rather than kWh, which means low power factor inflates your bill. Modern BESS inverters with reactive power capability can hold power factor near unity, reducing kVAh-billed units by 3-5% across the entire year, not just peak hours.

Diesel and outage displacement. For plants currently running diesel gensets during evening grid outages, a 4 MWh BESS provides roughly two hours of full-load backup at near-zero marginal cost compared to diesel at ₹20-25 per kWh.

Stacked, these three layers can add ₹25-30 lakh per year to a 2 MW plant’s Solar + BESS savings, on top of the headline ₹62 lakh peak-shift avoided cost.

Section 32 and the Tax Math

Section 32 of the Income Tax Act, 1961, treats solar generating systems including integrated storage as eligible for accelerated depreciation at 40% on Written Down Value. For a manufacturing or power-generating business, an additional 20% is available under Section 32(1)(iia) in the year the asset is first put to use, taking total Year One depreciation to 60% of the asset value.

A practical example for a 2 MW Solar + BESS project with a CapEx of ₹8 crore: Year One depreciation at 60% works out to ₹4.8 crore, which at the 25% corporate tax rate (applicable to most domestic companies under Section 115BAA) reduces tax outgo by roughly ₹1.2 crore. That is a Year One cash flow benefit equivalent to 15% of the project CapEx, before any operational savings.

Two important caveats. If the asset is commissioned after 3 October of a financial year, the Year One rate is halved (40% becomes 20%, and the additional 20% is also halved to 10%). Plan commissioning before this date to capture the full benefit. And the additional 20% under Section 32(1)(iia) is a one-time benefit available only in the first year the asset is put to use.

The Section 80-IA deduction for renewable power generation businesses, allowing 100% deduction of profits for ten consecutive years out of the first twenty years of operation, is also available for captive solar with storage. This requires more structured corporate planning to realise, typically through a separate Power-Plant SPV structure, but for plants with high evening-shift loads it is worth modelling.

How to Run This Past Your Audit Committee

Three questions will come up. Have clean answers ready.

How do we treat this on the books? Solar + BESS is a tangible fixed asset under Ind AS 16. Depreciation is per Section 32 of the Income Tax Act (40% WDV in Year One, 20% additional under 32(1)(iia), with the timing caveat above). The CERC IESS classification, while not directly governing behind-the-meter projects, gives auditors and lenders an unambiguous regulated-asset reference for valuation and useful life.

What is the hedge we are buying? You are simultaneously hedging three forward risks: ToD surcharge escalation, fossil-linked Fuel & Power Purchase Adjustment pass-throughs, and incremental grid charge introduction (Maharashtra’s GSC trigger is a precedent other states will likely follow). No financial instrument in the market offers a 15-year fixed-price hedge on industrial electricity. A captive Solar + BESS asset does.

What if tariffs drop? They will not drop in the peak window. The entire policy direction of MERC, KERC, GERC, and the Central Electricity Authority’s planning documents is to widen the peak-to-off-peak differential as renewable penetration grows. The only scenario in which your Avoided Cost shrinks is one in which India reverses ToD reform, which is not a base case any serious analyst is modelling.

The Decision Framework

You do not need to become an energy expert to make this call. You need to ask your team three questions and act on the answers.

What percentage of our electricity consumption falls inside the peak ToD window today, and what is the per-kWh differential we are absorbing on that block? Pull the last 12 months of HT bills. The answer will be obvious.

What is our current treatment of that peak-hour expense in our three-year budget? Most companies forecast it as fixed at last year’s rate. That is incorrect, and it understates the cost trajectory.

If we deployed a Solar + BESS asset sized to our peak-hour load profile, what would the IRR look like with and without the 40% accelerated depreciation in Year One? For most C&I operations in Maharashtra, Karnataka, Gujarat, Tamil Nadu, and Rajasthan in 2026, that IRR comes out at 18-24% post-tax, well above typical internal hurdle rates.

If the answer to the third question is above your hurdle rate, then continuing to buy peak-hour power from the grid is, in pure finance terms, a decision to keep writing cheques to hedge a risk you could retire.

The Avoided Cost Model is not an environmental argument. It is a reclassification of an OpEx liability into a CapEx asset, at a moment when the regulatory, technological, and financing environments have aligned to make that reclassification accretive.

Your board is going to ask about this in the next twelve months. Get there first.

How MGetEnergy Helps

MGetEnergy has been delivering Solar EPC and Hybrid + BESS solutions to C&I clients across India for 13+ years, with 45+ MWp delivered across 400+ installations including PSU clients like IOCL, GAIL, AIIMS New Delhi, Indian Air Force, and IWAI. Our engineering team designs solar-plus-storage systems sized to the specific load profile, ToD exposure, and tariff category of each plant, and our consulting practice provides plant-specific financial modelling that reflects current MERC, KERC, GERC, and other state tariff orders.

If your board or audit committee is evaluating Solar + BESS, we can support in three specific ways:

- A plant-specific Avoided Cost analysis using your last 12 months of HT bills and load curve data. This produces an audit-ready financial model rather than a vendor projection. Learn more about our Consulting & Feasibility services.

- Turnkey Solar + BESS engineering and execution under our Hybrid + BESS service line, with project sizes from 100 kW behind-the-meter retrofits to multi-MW captive installations.

- Zero-CapEx structured options through our PPA / Group Captive financing models for plants where the balance sheet does not permit upfront capital deployment.

To start a conversation, reach our team at wecare@mgetenergy.com or +91 98218 76325. Our offices in Delhi-NCR (Greater Noida) and Mumbai (Andheri East) handle pan-India C&I projects.

Frequently Asked Questions

Is BESS mandatory for industrial solar projects in India in 2026?

For new rooftop and grid-interactive solar projects above 100 kW commissioned in Maharashtra from 1 April 2026, yes. The Maharashtra Renewable Energy and Energy Storage Policy 2025-36 requires storage of at least 50% of renewable capacity with a two-hour minimum duration. Other states have not yet introduced similar mandates as of April 2026, but several are evaluating comparable frameworks. For existing installations, the mandate does not apply retroactively.

What is the realistic payback period for Solar + BESS in India?

For a well-designed C&I project with all annual benefit layers stacked (peak-hour avoided cost, demand charge reduction, kVAh billing optimisation, and outage displacement), payback in Maharashtra falls in the 6-8 year range against a 15-year asset life. Vendor quotes citing 4-5 year paybacks typically omit financing costs, battery degradation, and realistic O&M. Standalone Solar payback has stretched to 8-10 years post the same-slot banking restrictions.

What is the accelerated depreciation benefit for Solar + BESS under Indian tax law?

Section 32 of the Income Tax Act allows 40% Written Down Value depreciation in Year One on solar generating systems including integrated storage. An additional 20% is available under Section 32(1)(iia) for assets put to use in manufacturing or power generation, taking total Year One depreciation to 60%. If commissioned after 3 October of a financial year, the Year One rate is halved.

What is the Grid Support Charge in Maharashtra and why does it matter?

The Grid Support Charge is a per-kWh levy introduced by MERC under the Modified MYT Order, applicable to consumers in MSEDCL areas once the state’s rooftop solar capacity crossed 5,178 MW (which it did in 2025). The charge applies to all generated units, including self-consumed solar, and adds approximately ₹0.40 per kWh to the effective cost of grid-imported power. Stored energy from a BESS that offsets peak-hour grid import escapes this charge under the Maharashtra RE Policy 2025-36 grid charge exemption.

Can Solar + BESS qualify for VGF (Viability Gap Funding)?

The Ministry of Power’s second tranche VGF of ₹5,400 crore for 30 GWh of BESS, notified in June 2025 at ₹18 lakh per MWh, is reserved for utility-scale storage procured by states and NTPC under Tariff-Based Competitive Bidding. Behind-the-meter C&I projects do not access this scheme directly, but the scheme is driving down the system-level cost of battery cells and balance-of-system equipment, which flows through to C&I project pricing.

Does the CERC IESS framework apply to industrial Solar + BESS projects?

The Central Electricity Regulatory Commission’s Terms and Conditions of Tariff (Second Amendment) Regulations, 2026 (notified 20 March 2026) directly govern only Integrated Energy Storage Systems co-located with thermal generators or interstate transmission systems. Behind-the-meter C&I BESS projects are not directly regulated by this framework. However, the regulations create a regulated-asset template (15-year useful life, 14% base RoE, 85% round-trip efficiency) that lenders and auditors now reference when underwriting and valuing C&I storage projects.

References

This analysis draws from the following primary regulatory and policy sources:

- Maharashtra Electricity Regulatory Commission (MERC). Multi-Year Tariff Order, Case No. 217 of 2024, dated 28 March 2025. Approved Aggregate Revenue Requirement and tariff for the 5th Control Period FY 2025-26 to FY 2029-30 for MSEDCL.

- Maharashtra Electricity Regulatory Commission (MERC). Review of MYT Order, Case No. 75 of 2025, dated 25 June 2025. Modified MYT Order following review petition.

- Government of Maharashtra. Maharashtra Renewable Energy and Energy Storage Policy 2025-26 to 2035-36, Government Resolution dated 18 March 2026, in force until 31 March 2036.

- Central Electricity Regulatory Commission (CERC). Terms and Conditions of Tariff (Second Amendment) Regulations, 2026, notified 20 March 2026. Recognises Integrated Energy Storage Systems as a regulated asset class.

- Ministry of Power, Government of India. Operational Guidelines for the Scheme of Viability Gap Funding (VGF) for development of 30 GWh of Battery Energy Storage Systems, Order dated 10 June 2025. Total outlay ₹5,400 crore from Power System Development Fund.

- Ministry of Power, Government of India. Order on minimum 20% domestic content requirement for VGF-supported BESS projects, dated December 2025.

- Income Tax Act, 1961, Section 32 read with Appendix I of the Income Tax Rules. Depreciation rates as amended by Finance Act 2025.

- Central Electricity Authority (CEA). National Electricity Plan projections — 37 GWh of BESS capacity required by 2027, 236 GWh by 2031-32.

- GUVNL, RVUNL, MSEDCL, APTRANSCO, KPTCL, NVVN tender data for two-hour stand-alone BESS, 2024-2025. Cleared tariffs ranging ₹1.48 to ₹2.21 lakh per MW per month.

For plant-specific Avoided Cost modelling, finance teams should validate against their own load profile, voltage category, and applicable state tariff order. Figures cited are representative and reflect data available through April 2026.

Disclaimer: This article is for informational purposes and does not constitute financial, legal, or tax advice. Tariff orders, policy parameters, and tax provisions cited reflect the position as of April 2026 and may be revised by the issuing authority. Companies evaluating Solar + BESS investment decisions should consult a qualified Chartered Accountant for tax treatment specific to their situation, and validate plant-specific financial assumptions through detailed load-profile analysis.